Enrollment periods are critical for accessing health insurance plans, as they determine when individuals can apply for coverage. The two main types of enrollment periods are Open Enrollment and Special Enrollment, each serving different purposes and offering unique opportunities for members to enroll in health plans.

During these periods, individuals can assess their healthcare needs, compare available plans, and enroll in the coverage that best suits their circumstances. Whether during the annual Open Enrollment or a Special Enrollment triggered by a qualifying event, understanding these periods is crucial for securing timely health coverage.

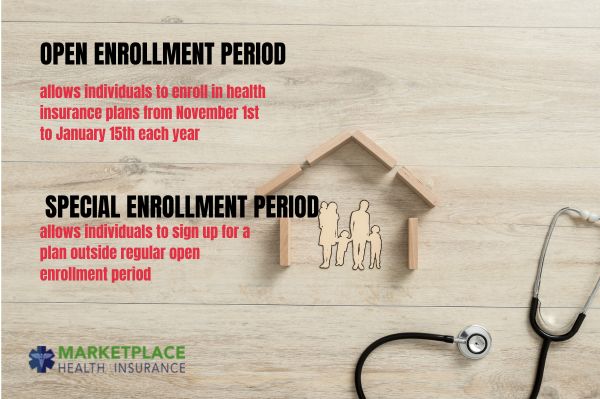

Open Enrollment

Open Enrollment is the designated period when individuals and families can enroll in Affordable Care Act plans without needing to provide proof of a qualifying life event. This period runs from November 1 to January 15, offering a window for consumers to apply for coverage or switch their existing plans.

During Open Enrollment, individuals can explore different health plan options, assess their healthcare needs, and make informed decisions about their coverage. This period is crucial for ensuring continuous health coverage and accessing necessary healthcare services without interruptions.

Special Enrollment Periods

Special Enrollment Periods allow individuals to enroll in health plans outside of the Open Enrollment period, provided they experience a qualifying life event. Common qualifying events include involuntary loss of coverage, gaining a dependent through birth or adoption, and permanent moves to areas with new health plans available.

Individuals typically have a 60-day window to enroll in a new health plan following a qualifying life event, and documentation proving the event is often required.

These periods ensure that individuals experiencing significant life changes can maintain their health coverage without gaps.

Who can enroll (Self- employed, unemployed, retired, have or offered a job-based insurance)

Various individuals can enroll in health plans during both Open and Special Enrollment periods, provided they meet eligibility criteria. Self-employed individuals, for instance, have the same enrollment options as others in the Marketplace.

Unemployed individuals who lose job-based insurance can enroll in a new plan through a Special Enrollment Period, ensuring they continue to have coverage. Retirees under 65 who lose their job-based health coverage are also eligible for a Special Enrollment Period to enroll in Marketplace plans.

Those with job-based insurance can explore Marketplace options if they find their current plan inadequate.